San Jose Rate Buydowns: When They Win (and How to Negotiate Them)

Home Buyer

Home Buyer

Rate buydowns can be a smart tool for San Jose buyers, but only when they are structured correctly.

The goal is not just to say you got a lower rate. The goal is to improve your monthly payment, protect your cash, negotiate more strategically, and avoid paying for a buydown that does not create enough real value.

In Silicon Valley, where home prices are high and monthly payment sensitivity is real, the way you structure your offer matters. A seller credit, a rate buydown, a lower purchase price, or a combination of all three can lead to very different outcomes.

This is why I do not look at rate buydowns in isolation. I look at the full buyer strategy: price, payment, cash to close, appraisal risk, loan guidelines, competition, and your long-term plan.

For a broader financing overview, I recommend reviewing our San Jose Home Loan & Mortgage Guide.

A rate buydown is when money is paid upfront to reduce the interest rate or reduce the buyer’s monthly payment for a period of time.

That money can come from:

In simple terms, a buydown is a way to trade upfront dollars for lower monthly payments.

For San Jose buyers, this can be helpful because affordability is often driven less by the purchase price alone and more by the monthly payment. A buyer may like the home, qualify for the loan, and have the down payment, but still feel pressure from the monthly payment.

A buydown can sometimes bridge that gap.

But it has to be analyzed carefully.

There are two common types of rate buydowns: temporary buydowns and permanent buydowns.

A temporary buydown lowers the buyer’s payment for a short period of time.

Common examples include:

A 2-1 buydown usually reduces the effective payment rate for the first year, then reduces it by a smaller amount in the second year, before the loan returns to the full note rate.

A 1-0 buydown usually reduces the effective payment rate for the first year only.

This can help buyers who want short-term payment relief, but it should not be used as a way to ignore the real long-term payment. You need to be comfortable with the full payment once the temporary buydown expires.

A permanent buydown usually means paying discount points to lower the interest rate for the life of the loan.

This can make sense when the monthly savings are meaningful and the buyer expects to keep the loan long enough to reach the break-even point.

The break-even point is one of the most important numbers. If the buydown costs $10,000 and saves $250 per month, the simple break-even point is about 40 months. If you sell, refinance, or pay off the loan before that point, the value may be limited.

That is why I always want buyers to compare the cost of the buydown against the actual monthly savings.

A rate buydown can make sense for San Jose buyers when it improves the overall purchase strategy.

It may be useful when:

This comes up often in the South Bay when a property is good but not perfect. Maybe the home needs updates. Maybe it missed the first wave of buyer attention. Maybe the seller overpriced it initially and is now more flexible.

In that situation, asking for a credit toward a buydown can sometimes create a better outcome than simply asking for a lower price.

A rate buydown does not automatically make every deal better.

It may not make sense when:

In San Jose, a great home in a strong neighborhood can still attract serious competition. In areas like Almaden Valley, Willow Glen, Cambrian, Berryessa, Evergreen, Santa Teresa, and parts of West San Jose, the best homes can move quickly when priced well.

In those situations, asking for a large seller credit may weaken your offer if other buyers are offering cleaner terms.

The key is knowing when to negotiate and when to compete.

A rate buydown can be paid by the buyer, the seller, or sometimes the builder.

A seller-paid buydown is often the most attractive structure for buyers because it uses seller credit to improve affordability.

This can work especially well when the seller is open to negotiation but does not want to reduce the purchase price further.

For example, a seller may prefer offering a credit instead of lowering the price because it helps preserve the recorded sale price. The buyer may prefer the credit because it can reduce the monthly payment more meaningfully than a small price reduction.

That is where negotiation strategy matters.

A buyer-paid buydown can make sense if the buyer has strong cash reserves and the break-even math is favorable.

But I do not like seeing buyers drain too much liquidity just to lower the payment slightly. In San Jose, buyers still need reserves for moving costs, repairs, furniture, property taxes, insurance, and unexpected expenses.

A lower rate is helpful, but being cash-poor after closing is not a win.

Builder-paid buydowns can be relevant when buying new construction. Builders may offer credits, rate incentives, or preferred lender programs.

These can be useful, but buyers should compare the incentive against the full price, upgrade costs, HOA costs, location, and resale value.

A builder credit is not automatically free money. It is part of the total negotiation.

A seller credit can sometimes be better than a price reduction, but not always.

The right answer depends on the numbers.

A lower purchase price reduces your loan amount, which can reduce your monthly payment. But in higher-priced San Jose purchases, a small price reduction may not move the monthly payment enough to solve the buyer’s real concern.

A seller credit, when allowed by the lender, may be used toward:

That can sometimes create more immediate payment relief or reduce the buyer’s cash needed to close.

For example, a buyer may be better off with a seller credit that lowers the monthly payment or preserves cash instead of a price reduction that only changes the payment slightly.

But this has to be reviewed with the lender because loan type, down payment, occupancy, appraisal, and credit limits all matter.

In San Jose, offer strategy is not just about price. It is about the full structure.

When I help buyers evaluate a buydown, I look at questions like:

A buydown may help on a home with less competition. It may not help on a home with multiple strong offers.

This is why buyers should not use the same strategy on every property. A strong offer in San Jose needs to match the home, the seller, and the current market conditions.

For a deeper look at the buying process, you can also review our San Jose Home Buying Process Guide.

Here is how I like buyers to approach rate buydowns before writing an offer.

Do not wait until after you find the house to ask about buydowns.

Before shopping seriously, ask your lender to show you:

This gives you a clearer strategy before you are under pressure.

If you are preparing to buy, our San Jose home buying page is a good place to start.

A buydown is not automatically worth it because the rate looks better.

You need to know:

This is where many buyers make a mistake. They focus on the lower rate instead of the real return on the buydown cost.

A seller is more likely to consider a credit when the property has some negotiation room.

That may include:

A seller is less likely to offer credits when the home is new to market, priced aggressively, and receiving strong interest.

Sometimes the best move is a seller credit.

Sometimes the best move is a lower purchase price.

Sometimes the best move is a mix of both.

The right structure depends on your payment goal, the seller’s motivation, the lender’s limits, and the appraisal risk.

This is where local experience matters. A strategy that works on a townhouse in one part of San Jose may not work on a single-family home in a highly competitive neighborhood.

A refinance can be a future option, but it should not be the only reason you buy today.

No one can guarantee future rates, future home values, or future lending conditions.

If a buydown helps you make the payment work today and the numbers make sense, that is different from buying only because you assume refinancing will solve the payment later.

I want buyers to be comfortable with the real payment, not just the hopeful future payment.

At Real Estate 38, we help buyers look at the full decision before writing offers.

That means comparing:

As Zaid Hanna, my role is not to tell every buyer to use a buydown. My role is to help you understand when it creates value and when it is just a distraction.

Sometimes a rate buydown is the right move.

Sometimes a lower price is better.

Sometimes preserving cash is more important.

Sometimes the cleanest offer wins.

That is why I like to run the numbers before we write, not after we are already in contract.

You can learn more about my local approach on my Zaid Hanna agent page, or you can reach out through our Real Estate 38 contact page.

Rate buydowns can be worth it for San Jose buyers when the monthly savings are meaningful, the break-even point makes sense, and the buyer expects to keep the loan long enough to benefit. They are especially useful when negotiated through seller credits on homes with less competition.

A temporary buydown lowers the buyer’s payment for a limited period of time, such as the first one or two years. A permanent buydown usually uses discount points to lower the interest rate for the life of the loan. Temporary buydowns help short-term affordability. Permanent buydowns are more focused on long-term savings.

You should ask the seller to pay for a rate buydown when the market conditions support it. This is more realistic on homes with longer days on market, price reductions, limited competition, or motivated sellers. It may be harder to negotiate on highly competitive San Jose homes with multiple offers.

A seller credit can be better than a price reduction when it improves the buyer’s monthly payment or reduces cash needed to close more effectively than a lower price. However, the lender must approve the credit structure, and the appraisal still needs to support the contract price.

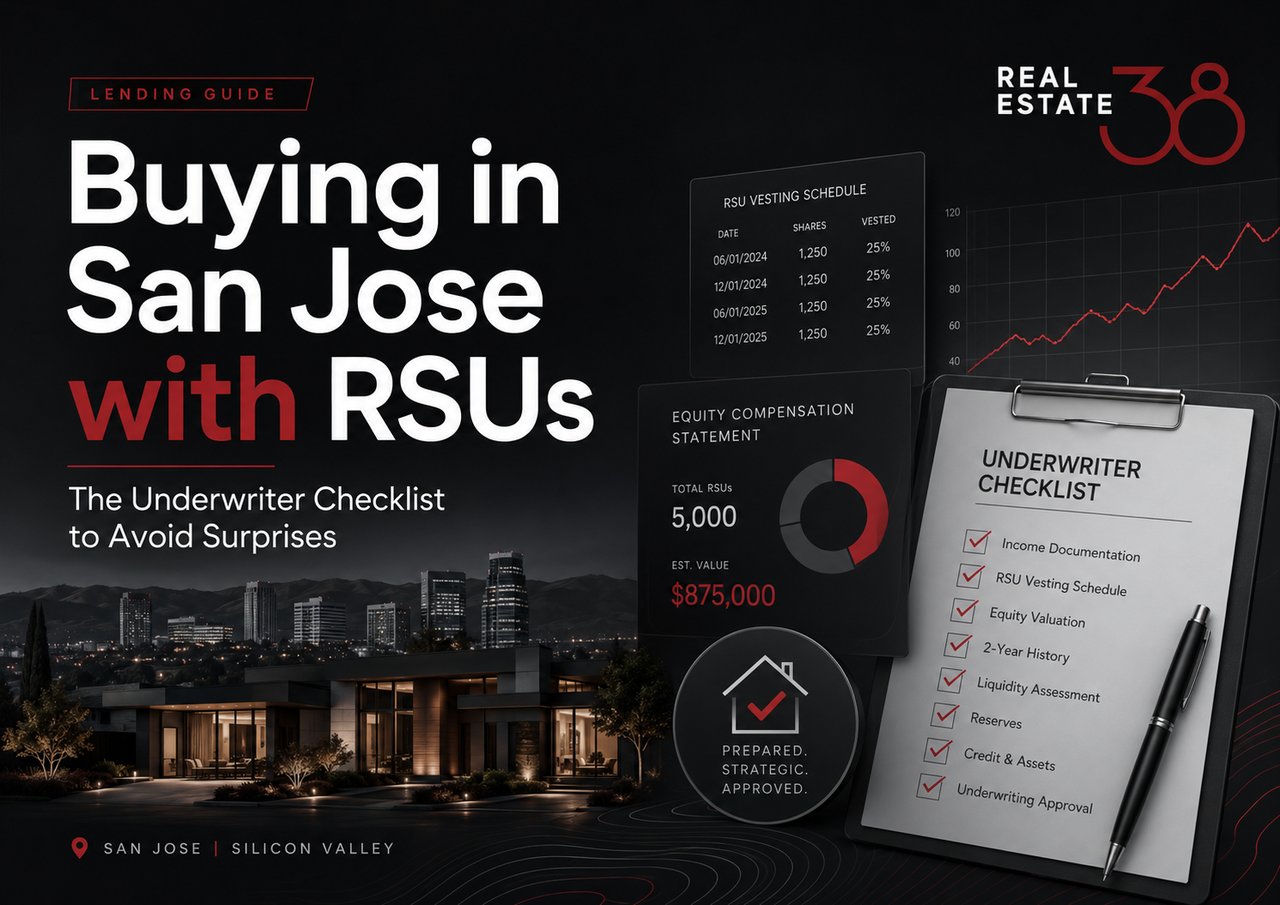

A rate buydown may improve monthly payment affordability, but it does not automatically mean you can qualify for a higher-priced home. Lenders may still qualify you based on the full note rate, loan program, debt-to-income ratio, down payment, and other guidelines. Always confirm with your lender before assuming a buydown increases your buying power.

Real Estate 38 helps San Jose buyers compare the real numbers before writing an offer. We look at purchase price, seller credits, monthly payment, lender guidelines, appraisal risk, days on market, seller motivation, and offer strength so the buyer can choose the structure that makes the most sense.

A rate buydown can be a powerful tool, but it is not a one-size-fits-all solution.

In San Jose and Silicon Valley, the best buyer strategy is the one that fits the home, the seller, the loan, and your long-term financial comfort.

Before you write an offer, make sure you know the difference between a lower rate, a better payment, a stronger offer, and a smarter negotiation.

Zaid Hanna

408-515-1613

www.re38.com

Stay up to date on the latest real estate trends.

July 14, 2026

July 6, 2026

July 2, 2026

June 29, 2026

June 27, 2026

June 22, 2026

You’ve got questions, and we can’t wait to answer them.