DTI Caps for San Jose Buyers: Why It Happens (and Fixes That Work)

Home Buyer

Home Buyer

I regularly meet San Jose buyers who earn strong incomes but are surprised by how little a lender says they can borrow.

This is especially common among Silicon Valley professionals with high base salaries, bonuses, commissions, RSUs, student loans, car payments, or other monthly obligations. On paper, their income may look excellent. During underwriting, however, the lender may calculate their financial position very differently.

The issue is often debt-to-income ratio, commonly called DTI.

DTI can cap your mortgage approval even when you have excellent credit, significant savings, and a strong career. The higher monthly payment attached to a San Jose home can push your ratio beyond a lender’s acceptable range faster than many buyers expect.

My goal is not simply to help you reach the highest approval amount possible. It is to help you understand your comfortable monthly payment, improve your buying power where appropriate, and enter the San Jose market with a financing and offer strategy that works together.

Debt-to-income ratio compares your qualifying monthly debt payments with the gross monthly income a lender is willing to use.

The basic calculation is:

Total monthly debt payments ÷ qualifying gross monthly income = DTI

For example, assume a lender counts the following:

The total DTI would be approximately 43.2%.

Lenders use DTI as one way to evaluate whether a borrower can manage the proposed mortgage payment alongside existing obligations. Different lenders and loan programs may apply different DTI limits.

You may hear a lender discuss two different ratios.

Front-end DTI generally compares the proposed housing expense with your qualifying gross monthly income.

The housing expense may include:

Back-end DTI includes the proposed housing expense plus other qualifying monthly debts, such as car loans, student loans, credit card payments, personal loans, and other mortgages.

The total or back-end ratio is usually the number buyers are referring to when they say they are being capped by DTI.

A high salary does not automatically create unlimited buying power.

A lender does not simply look at your annual compensation and multiply it by a standard number. The lender reviews how much of your income qualifies, how stable and documentable that income appears, and how much of it is already committed to recurring obligations.

A high-income San Jose buyer may still be capped because:

Fannie Mae’s automated underwriting system may permit total DTI ratios as high as 50% for certain casefiles, but that does not mean every borrower, lender, or loan will be approved at that level. Manually underwritten loans can have lower limits, and the overall risk profile still matters.

Your credit score, reserves, loan-to-value ratio, property type, occupancy, income stability, and loan size may all influence the final decision.

In San Jose, DTI is frequently a monthly payment problem rather than an income problem.

A buyer may earn $250,000, $350,000, or more per year and still feel restricted because the proposed payment on a South Bay property can absorb a large portion of qualifying monthly income.

The full housing payment may include:

A condominium with a lower purchase price may not produce the expected DTI improvement if it comes with a significant monthly HOA payment. A single-family home without an HOA may have a higher price but a different monthly cost structure.

Interest rates also affect this calculation. Even when the purchase price remains the same, a higher interest rate increases the monthly principal and interest payment. That can reduce the maximum loan amount a buyer qualifies for.

This is why I encourage buyers to evaluate homes by both price and monthly payment.

A lender may tell you the maximum amount you can borrow, but that is different from determining what you can comfortably afford while protecting your savings and other financial priorities. The Consumer Financial Protection Bureau also advises buyers to account for taxes, insurance, HOA dues, maintenance, and personal savings goals when evaluating affordability.

For a broader explanation of financing options and monthly payment planning, review my San Jose Home Loan and Mortgage Guide.

DTI is based more heavily on monthly required payments than on the total balance alone.

That distinction is important.

A $20,000 loan with a $900 monthly payment may hurt your buying power more than a much larger obligation with a lower qualifying payment. This is why paying down the right debt can sometimes help more than simply adding the same amount to your down payment.

A car payment can materially reduce mortgage capacity because it is added directly to your monthly obligations.

Vehicle leases can be especially important because lenders may treat the payment as recurring even when the current lease is close to expiring. The assumption is that the borrower will likely need another vehicle payment after the lease ends.

Student loan treatment depends on the loan program, repayment status, credit report, and available documentation.

A low payment shown on a statement may not always be the payment used for mortgage qualification. Deferred obligations may still need to be included in DTI under applicable guidelines.

Before assuming your student loan payment will have little impact, ask the lender exactly what monthly amount will be used.

For DTI purposes, the lender usually focuses on the required monthly payment rather than whether you pay the balance in full during a typical month.

Multiple credit cards with minimum payments can add up. Paying down or paying off a specific revolving balance may reduce the monthly obligation, but buyers should coordinate that decision with the lender before moving money.

Personal loans, furniture financing, buy-now-pay-later obligations, tax payment plans, and other installment debts may affect DTI.

Under Fannie Mae guidance, installment debts such as student loans, automobile loans, personal loans, and timeshares generally must be considered when enough monthly payments remain. Shorter-term debts may also be counted when the payment significantly affects the borrower’s ability to meet other obligations.

Co-signing for another person does not automatically remove the debt from your mortgage application.

Even when someone else makes the payment, the account may appear on your credit report and be included in your DTI unless the lender receives acceptable documentation showing that another party has consistently paid the obligation.

Current Fannie Mae guidance allows certain debts paid by others to be excluded when documentation requirements are satisfied, including evidence of an acceptable payment history.

Never assume a co-signed loan will be ignored.

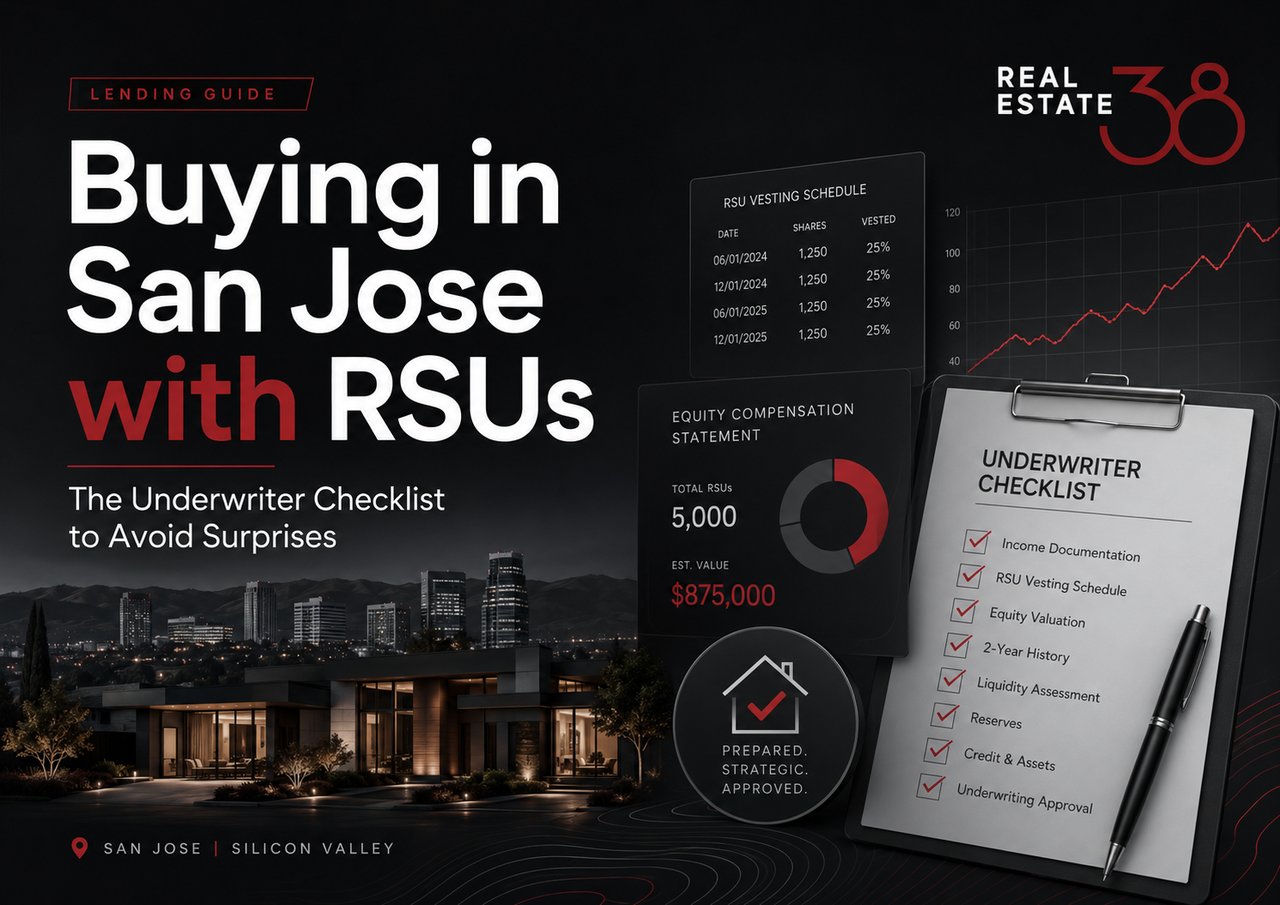

Many Silicon Valley buyers think about DTI using their total compensation package. The lender may use a smaller number.

That difference can dramatically change buying power.

Not every RSU grant will automatically count as qualifying income.

The lender may review:

For certain Fannie Mae loans, restricted stock generally must have vested and been distributed without restrictions before it can be treated as qualifying income. Documentation can include pay records, W-2s, vesting schedules, brokerage statements, and stock-price information.

A large unvested grant may be valuable to your long-term financial plan while contributing little or nothing to today’s mortgage qualification.

Bonus and commission income may be averaged rather than counted at the amount shown on your most recent paycheck.

The lender may analyze:

A buyer who expects a large bonus later in the year should not assume that future payment will immediately increase the current approval amount.

Self-employed income is often based on an underwriting analysis of tax returns and business cash flow, not gross revenue or deposits.

The lender may adjust for:

Business debt that is personally guaranteed can also affect the borrower’s total monthly obligations unless the lender can document that it is properly paid and accounted for by the business.

Rental income may help qualification, but lenders may not count every dollar of rent.

They may apply vacancy or expense adjustments and require leases, tax returns, appraisal forms, proof of deposits, or other documentation. The treatment can also depend on whether the property is currently rented, newly acquired, or being converted from a primary residence.

The lesson is simple: compensation and cash flow are not the same as qualifying income.

San Jose buyers frequently cross into jumbo financing because of local home prices and loan amounts.

A jumbo loan is not governed by one universal underwriting rulebook. Jumbo products can be portfolio loans, investor-specific programs, or loans with internal bank requirements.

Depending on the program, a jumbo lender may require:

This is where lender overlays matter.

An overlay is an additional requirement imposed by a lender beyond a broader loan program’s baseline eligibility rules. Two lenders reviewing the same buyer may calculate risk differently or offer different approval amounts.

That does not mean one lender is necessarily wrong. They may be offering different products or following different investor and risk requirements.

Before shopping, ask:

There is no single fix for every buyer. The right strategy depends on which side of the calculation is causing the problem.

Here are the areas I review with buyers and their lender.

Do not automatically pay off the debt with the largest balance.

Start by identifying which obligation creates the largest required monthly payment relative to the amount needed to eliminate it.

For example, using $20,000 to eliminate a $900 monthly payment may create more qualification improvement than adding that $20,000 to an already substantial down payment.

The lender should calculate the impact before you move the money.

Paying down a credit card may reduce the minimum payment and potentially improve credit utilization.

However, the timing of the new balance being reported can matter. Ask the lender whether a rapid rescore, updated statement, or other documentation is needed.

A co-signed obligation may be excludable when another party has made the payments and the lender receives acceptable documentation.

Do not wait until underwriting to collect payment records. Ask early what documents will be required.

A lender experienced with Silicon Valley compensation may identify eligible income that was not included in an initial online prequalification.

That does not mean income can be stretched or invented. It means documentation and program selection matter.

Prepare:

A conventional approval may produce a different result from a jumbo portfolio program. A lender that understands RSUs may calculate income differently from one that rarely works with Silicon Valley compensation.

Compare the entire approval, not just the advertised interest rate.

Review:

Sometimes the problem is not the loan. It is the monthly cost of the target property.

A buyer may improve affordability by adjusting:

This is where real estate and lending strategy need to be coordinated.

On the right property, a seller credit may be used toward eligible closing costs or an interest-rate buydown, subject to loan-program limits.

Lowering the interest rate can reduce the monthly payment and improve DTI. However, the value of a credit must be compared with negotiating a lower price.

The best choice depends on the loan, how long you expect to own the property, available cash, and the seller’s negotiating position.

Taking on a second job shortly before applying does not guarantee the income will count.

The lender may require a history of receiving that type of income. The same caution applies to newly created business income, future bonuses, projected rent, and unvested compensation.

Ask what can be documented before building your buying plan around it.

When buyers discover a DTI issue, they sometimes make rapid financial changes without understanding the underwriting consequences.

Before changing anything, avoid:

A well-intentioned move can create a new credit inquiry, reduce reserves, change the loan file, or fail to produce the expected DTI improvement.

Pre-approval should happen before serious home shopping, not after you find a property you want.

Our San Jose Home Buying Process Guide explains how financing preparation fits into the larger purchase timeline.

DTI does more than determine your maximum price. It affects how confidently and quickly you can compete.

A buyer operating close to the maximum allowable ratio may have less flexibility when:

Before writing an offer, I want to know:

A buyer approved at $1.8 million is not automatically prepared to offer $1.8 million on every property.

The payment and approval can change based on the specific home.

This is why I prefer property-specific payment reviews before my clients write offers, particularly when they are close to their DTI limit.

At Real Estate 38, I help San Jose buyers connect four decisions that are often treated separately:

I am not the mortgage underwriter, and I do not replace advice from a qualified loan professional. My role is to help make sure your financing strategy supports the type of offer we may need to write in the San Jose market.

Before we compete for a property, I help you evaluate:

You can learn more about my buyer representation approach on the Real Estate 38 buying page or review my background on the Zaid Hanna agent page.

There is no single ideal DTI for every San Jose buyer.

A lower DTI generally gives you more flexibility and may strengthen the overall risk profile. Some automated conventional approvals may permit a total DTI of up to 50%, while manual underwriting, jumbo products, and individual lenders may use lower limits.

Your comfortable DTI may also be lower than the lender’s maximum. The goal should be a payment that supports both homeownership and your other financial priorities.

The lender may be using less income than you expected or counting more monthly debt than you included in your own calculation.

Common causes include RSU restrictions, averaged bonus income, student loans, car payments, HOA dues, co-signed debt, self-employment adjustments, jumbo requirements, or lender overlays.

Ask the lender for a clear breakdown of the qualifying income and monthly obligations used.

Yes, paying off debt may improve DTI when it removes or reduces a monthly obligation.

The benefit depends on the required payment, payoff amount, remaining term, available reserves, and loan guidelines. Have the lender model the change before transferring funds.

RSUs may count when they meet the applicable loan program’s eligibility, documentation, history, and continuance requirements.

For certain Fannie Mae loans, restricted stock generally must have vested and been distributed without restrictions. Unvested grants and certain sign-on awards may not qualify.

The calculation may also depend on whether the award is time-based or performance-based and whether it is paid in cash or shares.

They can be.

Jumbo lenders may establish their own requirements for DTI, reserves, credit, income history, post-closing liquidity, and variable compensation. Because jumbo programs differ, buyers should compare more than one appropriate lending option.

I help buyers coordinate the property search with their financing limits.

We compare the approved price, comfortable payment, property taxes, HOA dues, potential seller credits, and offer terms before writing. When a DTI issue appears, I work with the buyer and lender to understand the available options without pushing the buyer beyond a responsible budget.

If your income looks strong but your mortgage approval feels unexpectedly limited, do not assume the answer is simply to earn more or abandon your home search.

The restriction may come from one monthly payment, an incomplete income calculation, a lender overlay, the wrong loan program, or a property cost that was not included in the original estimate.

The best time to identify those issues is before you fall in love with a home.

I can help you connect your financing position with a realistic San Jose property search and offer strategy. To begin, use the Real Estate 38 contact page or reach me directly.

Zaid Hanna

408-515-1613

www.re38.com

Stay up to date on the latest real estate trends.

July 14, 2026

July 6, 2026

July 2, 2026

June 29, 2026

June 27, 2026

June 22, 2026

You’ve got questions, and we can’t wait to answer them.