How Do Rate Buydowns Work in San Jose? (2026 Guide)

After learning how mortgage rates work, many buyers ask:

“Can I lower my rate?”

“What is a 2-1 buydown?”

“Are buydowns worth it?”

“Should I pay points?”

In San Jose’s higher price ranges, even small interest changes affect monthly payments significantly.

This guide explains what rate buydowns are, how they work, and when they make sense in 2026.

For a full overview of financing options, start here:

👉 https://re38.com/san-jose-home-loan-mortgage-guide

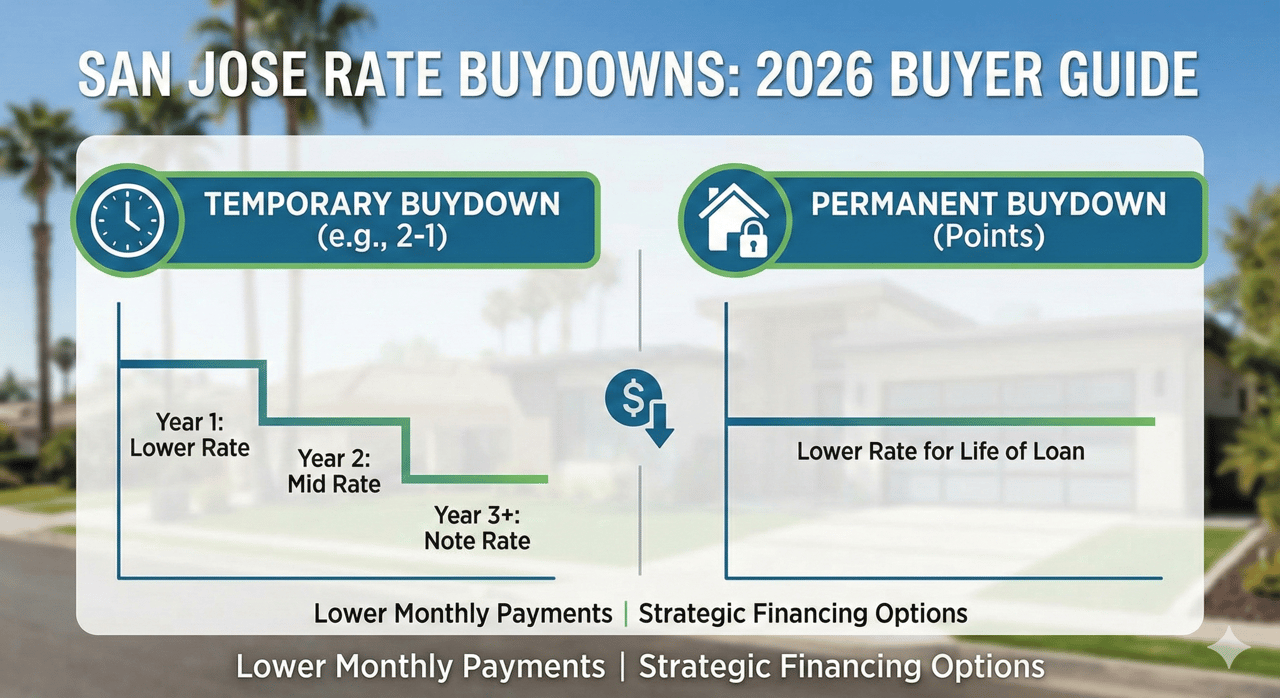

A rate buydown is when a buyer (or sometimes a seller) pays upfront to reduce the mortgage interest rate.

There are two main types:

Rate is reduced for the first 1–2 years

Payment gradually increases later

Often seller-funded

Buyer pays upfront “points”

Rate is reduced for the entire loan term

Long-term savings if you stay in the home

Example:

If the note rate is 6.5%:

Year 1 = 4.5%

Year 2 = 5.5%

Year 3 onward = 6.5%

This reduces early monthly payments — often helpful for:

first-time buyers

buyers expecting income growth

buyers planning to refinance

For rate basics, review:

👉 https://re38.com/blog/how-do-mortgage-rates-work-and-what-affects-them-san-jose

Buydowns can be paid by:

the buyer

the seller (as a concession)

the builder (new construction)

In 2026, seller-funded buydowns are common when:

inventory increases

homes sit longer

sellers want to attract buyers

For seller timing context, see:

👉 https://re38.com/blog/how-long-will-it-take-to-sell-my-home-san-jose

Permanent buydowns make sense when:

you plan to stay long-term

you don’t expect to refinance soon

you have extra cash at closing

break-even math supports it

If you refinance quickly, paying points may not pay off.

Some buyers wonder:

“Should I buy down my rate or put more down?”

Both strategies reduce monthly payments, but differently:

Down payment lowers loan balance

Buydown lowers interest rate

The right choice depends on:

cash reserves

long-term plans

overall affordability

For down payment context, review:

👉 https://re38.com/blog/how-do-down-payments-actually-work-san-jose

Buydowns are not automatically good or bad.

Buyers should:

calculate break-even timelines

compare lender quotes

consider refinance plans

understand full closing costs

In 2026:

buydowns are common negotiation tools

seller concessions are more flexible than frenzy years

payment strategy matters more than chasing rate predictions

Smart buyers focus on overall payment structure, not just the headline rate.

Before deciding on a buydown, it helps to:

understand your affordability

review loan options

compare scenarios

calculate break-even points

I help buyers:

evaluate buydown options

structure financing strategically

avoid paying for benefits they won’t use

👉 If you want to compare payment scenarios, reach out here:

https://re38.com/contact

You don’t need to guess or rely on internet calculators.

A short conversation can help you understand whether a buydown improves your position — or if another strategy makes more sense.

Zaid Hanna

408-515-1613

www.re38.com

Stay up to date on the latest real estate trends.

August 6, 2026

July 31, 2026

July 27, 2026

July 24, 2026

July 24, 2026

July 22, 2026

You’ve got questions, and we can’t wait to answer them.