How Much Do I Need for a Down Payment to Buy a Home in San Jose?

Home Loans, Mortgage Rates & Affordability Guide

Home Loans, Mortgage Rates & Affordability Guide

One of the biggest misconceptions I hear from buyers is:

“I need 20% down to buy a home in San Jose.”

That belief stops many qualified buyers from even starting the conversation — especially in a high-priced market like ours.

The reality is: there is no single “required” down payment amount.

Your ideal down payment depends on your goals, loan type, income structure, monthly comfort, and long-term strategy.

This guide breaks down the real down payment options available in San Jose and explains when putting less down can actually make sense.

For a full overview of financing options, start here:

👉 https://re38.com/san-jose-home-loan-mortgage-guide

Twenty percent down helps you avoid PMI, but it is not required for most conventional loans — even in San Jose.

What matters more is:

affordability

monthly payment comfort

loan structure

long-term plan

Here’s how most buyers structure their down payments:

First-time buyers

Strong credit profiles

Conventional loans

PMI required

Best for buyers who want to enter the market sooner.

Very common in San Jose

Balanced approach

Lower PMI than 5%

Keeps more cash available

Often ideal for tech buyers.

Reduces or eliminates PMI

Lower monthly payment

Stronger offer profile

Preferred by move-up buyers.

No PMI

Lowest monthly payment

Best for long-term holds

Common for equity-rich buyers or those using RSUs.

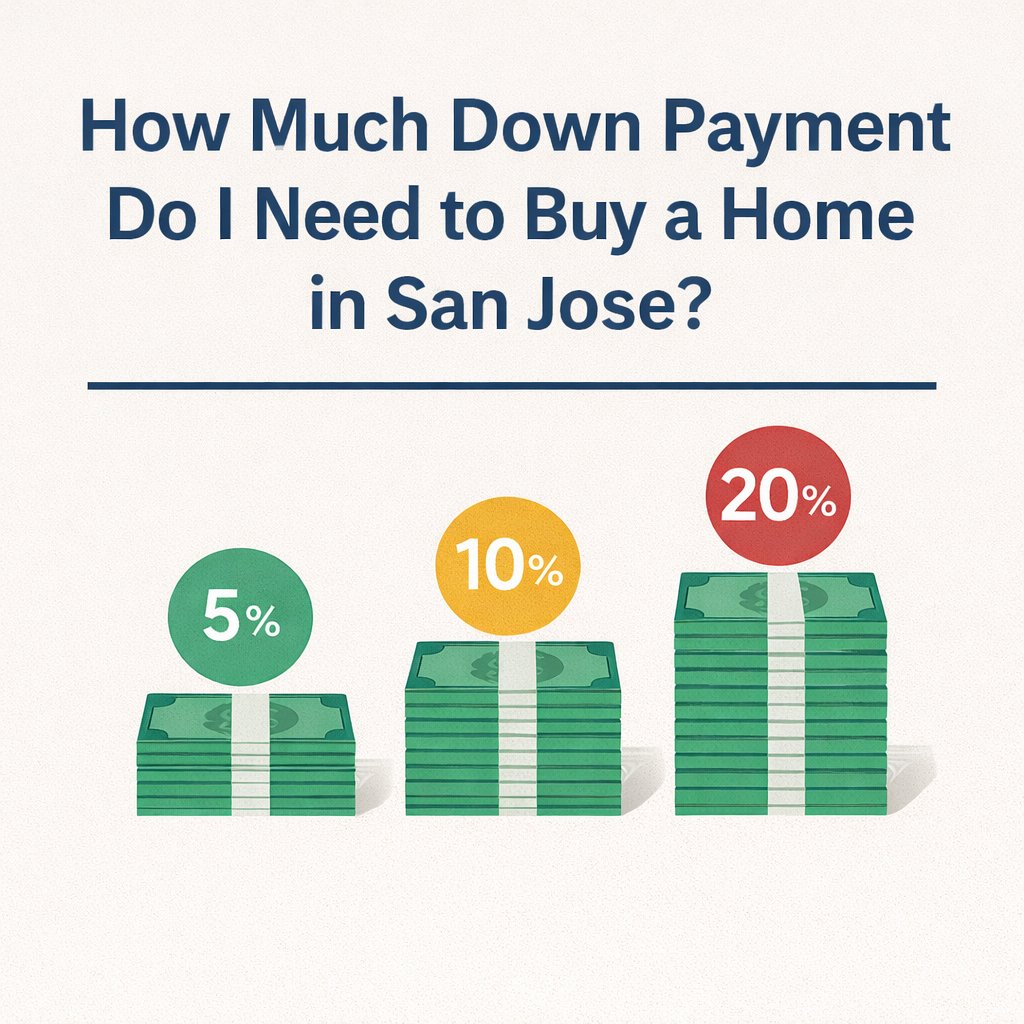

Let’s translate percentages into real numbers.

5% down = $60,000

10% down = $120,000

20% down = $240,000

5% down = $80,000

10% down = $160,000

20% down = $320,000

Seeing it this way helps buyers realize that waiting to save 20% can delay ownership by years.

PMI (Private Mortgage Insurance):

protects the lender

applies when down payment is under 20%

is not permanent

In many cases:

PMI costs less than expected

PMI can be removed once you reach 20% equity

appreciation in San Jose can accelerate removal

Paying PMI for a few years is often cheaper than waiting on the sidelines.

Putting less down can be smart if:

you have strong income

your monthly payment is comfortable

you want to keep cash for:

reserves

investments

remodeling

emergencies

Many San Jose buyers prefer liquidity over tying up all their cash in a down payment.

A larger down payment may be better if:

you want the lowest possible payment

you’re rate-sensitive

you’re buying long-term

you want to avoid PMI

you’re using proceeds from a sale

There’s no “right” answer — only what fits your strategy.

In San Jose, many purchases fall into jumbo loan territory.

Jumbo loans often:

require higher down payments (10–20%)

have stricter reserve requirements

offer competitive rates for strong borrowers

This is why structuring your down payment with the right lender is critical.

Remember, you also need funds for:

closing costs

inspections

appraisal

reserves

A smart plan balances:

down payment

monthly payment

cash reserves

For the full buying roadmap, review:

👉 https://re38.com/san-jose-home-buying-process-guide

Instead of guessing how much you need, let’s look at your numbers together.

We’ll review:

income and bonuses/RSUs

credit profile

loan options

monthly comfort level

down payment scenarios

what homes fit your budget

👉 Reach out here:

https://re38.com/contact

A quick conversation can help you understand your real options and create a plan that works — without pressure.

Zaid Hanna

408-515-1613

www.re38.com

Stay up to date on the latest real estate trends.

August 6, 2026

July 31, 2026

July 27, 2026

July 24, 2026

July 24, 2026

July 22, 2026

You’ve got questions, and we can’t wait to answer them.