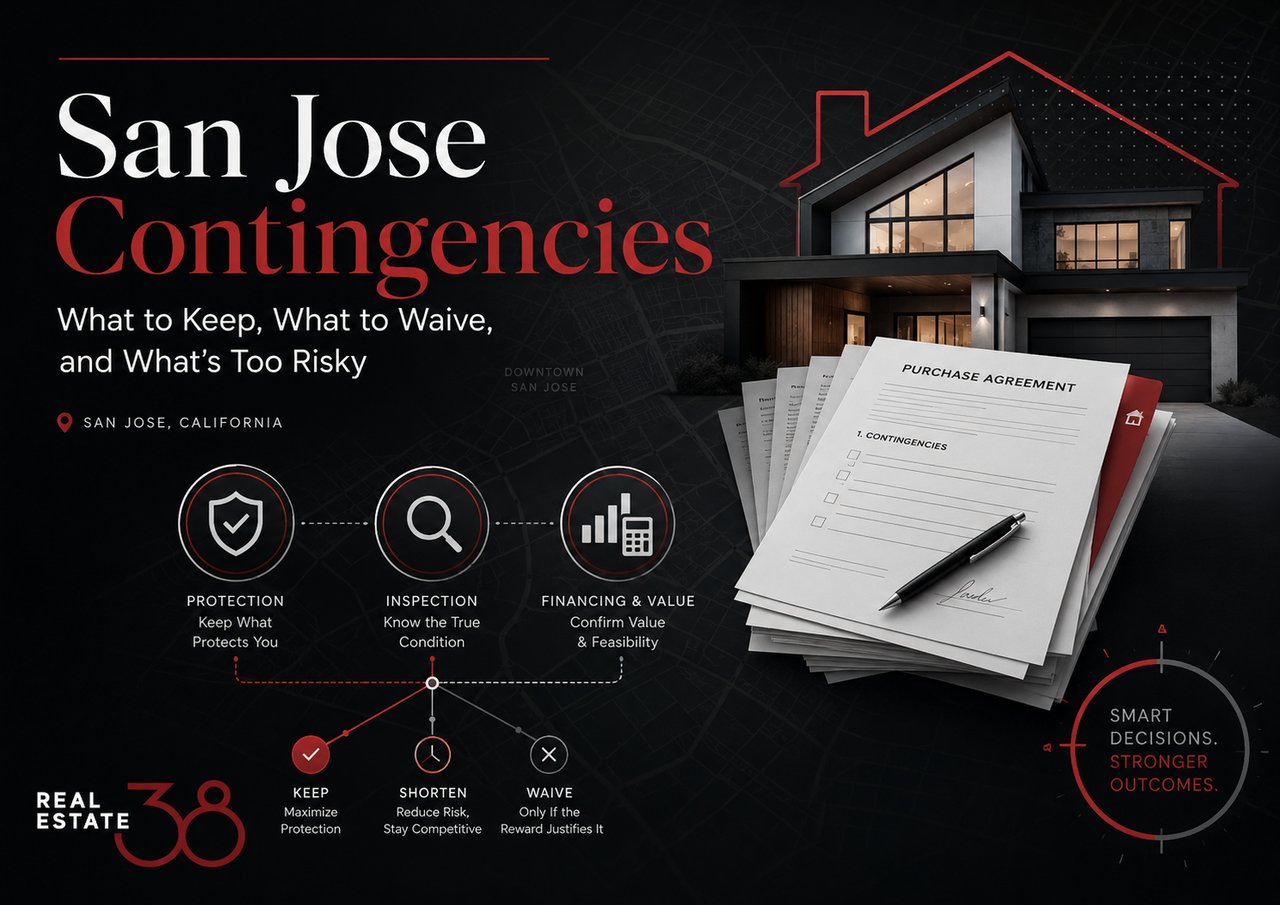

San Jose Contingencies: What to Keep, What to Waive, and What’s Too Risky

Home Buyer

Home Buyer

When you are buying a home in San Jose, your offer is not just about price.

The terms matter.

One of the biggest parts of your offer strategy is how you handle contingencies. Contingencies can protect you as a buyer, but they can also make a seller nervous if they feel your offer has too many ways to fall apart.

That is why I never tell buyers to blindly waive everything just to “win.” That is not strategy. That is gambling.

The right contingency plan depends on the home, the disclosure packet, the inspection reports, your financing, the appraisal risk, the level of competition, and your comfort level. My job is to help you compete while still understanding what risk you are taking.

If you are preparing to buy in San Jose, start with our full San Jose Home Buying Process Guide here:

https://re38.com/san-jose-home-buying-process-guide

A contingency is a condition that must be satisfied for the purchase to move forward.

In simple terms, contingencies give buyers time to investigate the property, confirm financing, review the appraisal, and decide whether they are comfortable proceeding.

Common buyer contingencies include:

Inspection contingency

Appraisal contingency

Loan contingency

Review of disclosures

Review of HOA documents for condos and townhomes

Title review

Sale-of-home contingency, when applicable

In a competitive San Jose market, sellers usually want certainty. They want to know that once they accept your offer, the deal is likely to close.

That is why contingencies matter so much. They affect how strong or risky your offer looks from the seller’s side.

From a seller’s perspective, every contingency is a potential exit point.

If the buyer has an inspection contingency, the buyer may cancel after reviewing the property condition. If the buyer has an appraisal contingency, the buyer may renegotiate or cancel if the appraisal comes in low. If the buyer has a loan contingency, the seller may worry about whether the buyer’s financing is truly solid.

This does not mean contingencies are bad. It means they need to be handled carefully.

A seller is asking themselves:

Will this buyer close?

Will they come back asking for credits?

Will they cancel after inspections?

Will the lender perform?

Will the appraisal become a problem?

Is this offer clean enough compared to the other offers?

In San Jose, where many homes receive multiple offers, a buyer with a cleaner, better-prepared offer can sometimes beat a higher offer if the seller believes it is more likely to close.

That is why the strongest offer is not always the highest price. It is often the offer with the best combination of price, certainty, preparation, and risk management.

For more guidance on buying in San Jose, visit:

Contingencies affect offer strength because they change the seller’s confidence level.

A long contingency period usually gives the buyer more protection, but it may make the seller feel exposed. A shorter contingency period may make the offer stronger, but it gives the buyer less time to investigate. A waived contingency may make the offer more competitive, but it can also create serious financial risk if the buyer is not fully prepared.

This is where strategy matters.

Sometimes the best move is not to waive a contingency. Sometimes the better move is to shorten the timeline, provide stronger supporting documents, use a great lender, review disclosures thoroughly before writing, and structure the offer in a way that gives the seller confidence without putting the buyer in a dangerous position.

The inspection contingency gives you time to evaluate the condition of the home.

This can include the general home inspection, roof, foundation, drainage, electrical, plumbing, HVAC, pest issues, permits, safety concerns, and any visible or reported defects.

In San Jose, this is especially important because we see a wide range of property types and conditions. A newer condo in a managed community is very different from an older single-family home in Willow Glen, Cambrian, Berryessa, Evergreen, Rose Garden, Almaden Valley, or Downtown San Jose.

A home may look beautiful online, but the real risk is often in the details.

The inspection contingency matters most when the property has unknowns.

I pay close attention when a home is:

Older

Remodeled

Expanded or modified

Sold by a trust or estate

Missing permits

Showing signs of drainage issues

Showing foundation movement

Located on a slope

A condo or townhome with HOA concerns

A property with additions, converted spaces, or garage modifications

A remodeled home can still have issues behind the walls. A beautiful kitchen does not automatically mean the electrical, plumbing, roof, drainage, or foundation are in great condition.

This is why I want my buyers to review the disclosure packet, inspection reports, seller disclosures, permit history when available, HOA documents when applicable, and any known property concerns before deciding what to do with the inspection contingency.

Before you shorten or waive an inspection contingency, you should know what you are relying on.

At minimum, I want my buyers to review:

The seller disclosures

The property inspection report

The termite or pest report

Roof information, if available

Foundation comments, if any

Permit information, when available

HOA documents for condos and townhomes

Natural hazard disclosures

Any known repairs or insurance claims

Comparable property condition in the area

If the disclosure packet is strong and complete, the buyer may feel more comfortable shortening the contingency period. If the disclosure packet is weak, incomplete, vague, or missing key reports, waiving inspection may be too risky.

The appraisal contingency protects the buyer if the home does not appraise at the purchase price.

This matters because lenders usually base the loan on the lower of the purchase price or appraised value. If the appraisal comes in low, the buyer may need to bring in more cash, renegotiate, or cancel if they have the right protection in place.

For example, if you offer $1,500,000 and the home appraises at $1,450,000, there is a $50,000 appraisal gap. Depending on your loan structure, that gap may need to be covered with additional cash.

That is why appraisal risk must be evaluated before writing the offer, not after.

In competitive San Jose situations, appraisal gap language can sometimes help.

This means the buyer may agree to cover a certain amount of difference between the appraised value and the purchase price.

For example, instead of fully waiving the appraisal contingency, a buyer might say they are willing to cover up to a specific dollar amount if the appraisal comes in low.

This can give the seller more confidence while still placing a limit on the buyer’s risk.

But this only works if the buyer has the cash to support it. Appraisal gap language should never be used casually. It needs to be coordinated with the lender, reviewed against the buyer’s cash reserves, and evaluated against comparable sales.

The loan contingency protects the buyer if they cannot obtain financing under the agreed terms.

In San Jose, financing strength is a major part of offer strategy. Sellers and listing agents want to know that the buyer is truly qualified, not just casually pre-approved.

A strong pre-approval can make a major difference.

The quality of the lender matters too. A responsive, reputable lender who communicates clearly with the listing agent can reduce seller concern. If the lender can explain the buyer’s qualifications, income review, asset review, credit strength, and ability to close, the offer becomes stronger.

A weak pre-approval letter from a lender who does not answer calls can hurt the offer, even if the price is good.

Not all pre-approvals are equal.

Some buyers are pre-qualified based on basic information. Others are fully underwritten or much further along in the approval process.

When I help buyers compete, I want to understand:

Has the lender reviewed income?

Has the lender reviewed assets?

Has the lender reviewed credit?

Has the lender reviewed debt-to-income ratio?

Has the buyer’s cash to close been verified?

Can the lender call the listing agent?

Can the lender close on the proposed timeline?

This matters because the more confidence we can give the seller, the less scary the financing contingency becomes.

In San Jose, many listing agents provide disclosure packets before offers are due.

This can include inspections, seller disclosures, HOA documents, preliminary title reports, natural hazard reports, and other property information.

A strong disclosure packet helps buyers make better decisions before writing an offer.

But not all disclosure packets are equal.

Some are detailed and organized. Some are missing key reports. Some raise more questions than answers. Some disclose past repairs but do not provide enough documentation. Some include HOA information that needs careful review.

This is why I do not treat every property the same. The disclosure packet is one of the biggest factors in deciding whether a buyer should keep, shorten, modify, or waive a contingency.

A condo buyer and a single-family home buyer may need very different contingency strategies.

For condos and townhomes, I want buyers to pay close attention to:

HOA dues

HOA reserves

Rental restrictions

Special assessments

Insurance coverage

Litigation

Maintenance responsibilities

Parking and storage

Rules and restrictions

Pending repairs or community issues

For older single-family homes, I look closely at:

Foundation

Drainage

Roof

Electrical systems

Plumbing

Sewer lines

Pest damage

Permit history

Additions and remodels

Signs of deferred maintenance

For remodeled homes, I want to know whether the work was permitted, whether it was done properly, and whether the improvements match what buyers are paying for.

For homes with additions, converted garages, or expanded living areas, buyers need to be extra careful. A home may have more usable space than the tax records show, but that does not always mean the work was permitted or completed correctly.

In many cases, shortening a contingency can be a smarter strategy than waiving it.

For example, instead of asking for 10 or 17 days for inspections, a buyer may shorten the inspection contingency to a few days if they can review disclosures quickly and schedule follow-up inspections immediately.

This can make the offer more attractive while still giving the buyer a defined window to investigate.

The same idea can apply to loan or appraisal contingencies, depending on the lender, the property, and the buyer’s financial strength.

Shortening a contingency says, “We are serious and prepared.”

Waiving a contingency says, “We are taking the risk.”

Those are not the same thing.

Waiving a contingency may be too risky when the buyer does not fully understand the downside.

I get especially cautious when:

The disclosure packet is incomplete

The home is older or has visible concerns

The buyer has limited cash reserves

The buyer is stretching financially

The appraisal risk is high

The lender has not fully reviewed the file

The property has additions or permit questions

The HOA documents raise concerns

The buyer is uncomfortable with the risk

The competition is pushing the buyer into emotional decisions

A strong offer should still be a smart offer.

Winning the house does not help if the buyer later realizes they accepted a risk they were not prepared to handle.

Earnest money is another reason contingencies matter.

When buyers remove or waive protections, their deposit may be more exposed if they later cancel without a valid remaining contingency.

That is why I want buyers to understand the connection between contingencies and earnest money before they write the offer.

This is not something to figure out after acceptance. It needs to be discussed upfront.

Before removing a contingency, the buyer should understand what they are giving up, what risk remains, and what could happen if they cannot or do not want to close.

You can compete in San Jose without blindly waiving everything.

A strong offer can include:

A well-vetted pre-approval

A lender who communicates with the listing agent

A clean and organized offer package

Proof of funds

A realistic closing timeline

A thoughtful inspection strategy

A clear appraisal strategy

A strong understanding of disclosures

A competitive price backed by comparable sales

A confident but reasonable negotiation plan

Sometimes the best way to strengthen an offer is preparation, not recklessness.

At Real Estate 38, we help buyers evaluate risk before they write the offer.

That means we review the property, the disclosures, the inspection reports, the comparable sales, the lender input, and the local market dynamics before recommending a strategy.

When I advise a buyer, I am looking at questions like:

How competitive is this home likely to be?

Are there multiple offers?

Is the property priced low to attract bidding?

Do the comparable sales support the offer price?

Is there appraisal risk?

Are the disclosures complete?

Are there condition concerns?

Is the buyer financially strong enough to absorb certain risks?

Can we shorten a contingency instead of waiving it?

Is there a smarter term that gives the seller confidence without overexposing the buyer?

This is where local experience matters. San Jose is not one market. A condo near Santana Row, a townhome in North San Jose, a single-family home in Cambrian, a hillside property in Almaden Valley, and an older home in Willow Glen can all require different strategies.

There is no universal answer to what you should keep, shorten, or waive.

The right strategy depends on:

The home

The disclosures

The inspection reports

The buyer’s financing

The buyer’s cash reserves

The appraisal risk

The number of competing offers

The seller’s priorities

The buyer’s comfort level

My advice is simple. Do not make contingency decisions based on fear. Make them based on preparation, data, and clear risk evaluation.

If you are serious about buying a home in San Jose, talk through the contingency strategy before you write the offer.

Not after.

A good strategy can help you protect yourself, compete more effectively, and avoid giving up protections that are not worth sacrificing.

If you are preparing to buy in San Jose, start here:

https://re38.com/san-jose-home-buying-process-guide

You can also learn more about how we help buyers here:

And when you are ready to talk through a specific home or offer strategy, contact us here:

The goal is not just to win the home. The goal is to win the right home with the right terms and the right level of protection.

For more guidance, learn about buying a home in San Jose, explore current homes for sale, compare San Jose neighborhoods, or meet Zaid Hanna and the Real Estate 38 team.

Zaid Hanna

408-515-1613

www.re38.com

Stay up to date on the latest real estate trends.

June 27, 2026

June 22, 2026

June 15, 2026

June 10, 2026

June 8, 2026

June 5, 2026

You’ve got questions, and we can’t wait to answer them.