Low Appraisal in San Jose: The Buyer Playbook to Stay Protected

Home Buyer

Home Buyer

A low appraisal can change the entire conversation when you are buying a home in San Jose.

One minute, you are excited because your offer was accepted. The next minute, the lender says the home did not appraise at the purchase price, and now you have to figure out what that means for your loan, your cash to close, your earnest money, and your ability to move forward.

This is why I talk about appraisal risk before my buyers write an offer, not after.

In San Jose real estate, the right offer strategy is not just about how much you offer. It is about understanding the home, the comparable sales, the competition, your financing, your cash reserves, and your protection level before you put your money on the line.

If you are preparing to buy a home in San Jose, start with our full San Jose Home Buying Process Guide here: https://re38.com/san-jose-home-buying-process-guide

A home appraisal is the lender’s opinion of the property’s value.

When you buy a home with a mortgage, the lender wants to make sure the property is worth enough to support the loan. The lender is not simply lending based on what you offered. They are lending based on the lower of the purchase price or the appraised value.

That difference matters.

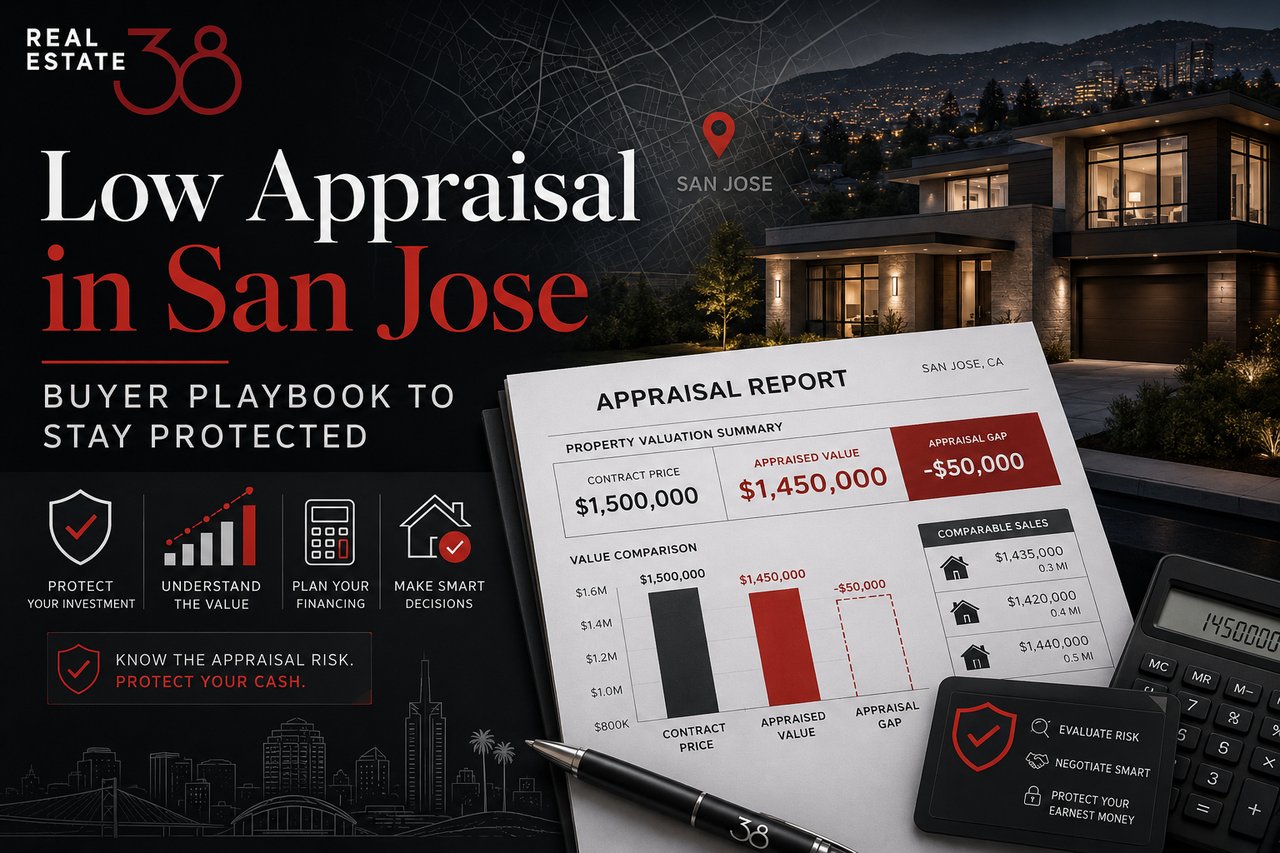

If you offer $1,500,000 on a San Jose home and the appraisal comes in at $1,450,000, the lender will usually base the loan on $1,450,000, not $1,500,000.

That $50,000 difference is the appraisal gap.

An appraisal gap is the difference between the contract price and the appraised value.

Example:

Purchase price: $1,500,000

Appraised value: $1,450,000

Appraisal gap: $50,000

The lender may still approve the loan, but the buyer may need to bring more cash to close, renegotiate with the seller, restructure the financing, dispute the appraisal, or cancel if protected by the contract.

This is why appraisal strategy matters so much in San Jose.

Low appraisals happen when the appraiser’s supported value comes in below the purchase price.

In San Jose, this can happen for several reasons:

This is especially common in fast-moving neighborhoods where buyer demand is strong, inventory is limited, and the best homes attract multiple offers.

This is one of the biggest things buyers need to understand.

The list price is the seller’s marketing price.

The purchase price is what the buyer and seller agree to.

The appraised value is what the lender’s appraiser supports.

The true market value is what qualified buyers are willing to pay in the current market.

In San Jose, these numbers can be different.

A home may be listed at $1,399,000, receive multiple offers, go into contract at $1,520,000, and appraise at $1,475,000. That does not automatically mean the buyer overpaid. It means the market and the appraisal process may be looking at the home from different angles.

My job is to help buyers understand that difference before they decide how aggressive they want to be.

A low appraisal can affect the buyer’s loan because the lender usually calculates the loan amount based on the appraised value, not the contract price.

Let’s say a buyer plans to put 20% down on a $1,500,000 purchase.

Expected down payment: $300,000

Expected loan amount: $1,200,000

But if the appraisal comes in at $1,450,000, the lender may base the 80% loan on $1,450,000 instead.

New loan amount: $1,160,000

Original contract price: $1,500,000

Cash needed to close: $340,000

That buyer may now need an additional $40,000 in cash compared to what they expected.

This is why buyers should never look only at the down payment percentage. They need to understand what happens if the appraisal comes in low.

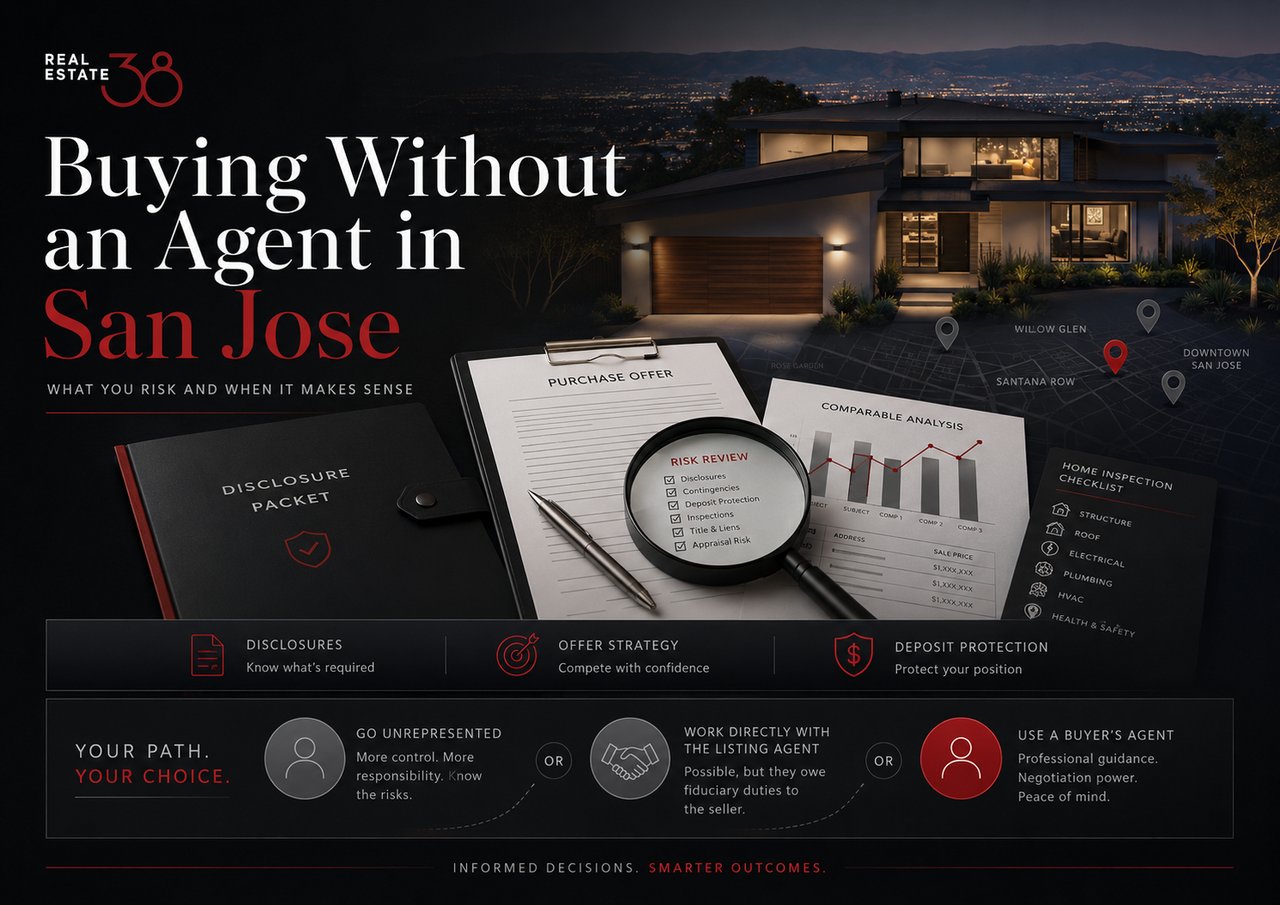

An appraisal contingency gives the buyer a contractual protection if the home does not appraise at the purchase price.

If the appraisal comes in low and the buyer has an appraisal contingency, the buyer may have options, depending on the contract terms and timelines. Those options may include renegotiating the price, asking the seller to reduce the price, bringing in additional cash, or canceling the contract and protecting the earnest money deposit.

This does not mean every buyer should always keep every contingency in every situation. It means the buyer should understand exactly what they are risking before removing one.

For a broader look at the buying process, contingencies, and offer strategy, visit: https://re38.com/buying

Waiving the appraisal contingency can make an offer more attractive to a seller, but it can also increase the buyer’s risk.

It may be risky when:

I do not believe in telling buyers to waive protections blindly. That is not strategy. That is guessing.

The right decision depends on the home, the competition, the comparable sales, the financing, and the buyer’s comfort level.

Sometimes, a buyer may use appraisal gap language instead of fully waiving appraisal protection.

For example, a buyer may say they are willing to cover an appraisal gap up to a certain amount.

That can make an offer stronger because it gives the seller more confidence, while still giving the buyer a defined limit.

Example:

Offer price: $1,500,000

Buyer agrees to cover appraisal gap up to: $30,000

If the home appraises at $1,470,000, the buyer can move forward

If the home appraises much lower, the buyer may still have protection depending on the contract language

This type of strategy can be useful when the buyer wants to compete but does not want unlimited exposure.

The wording matters. The amount matters. The financing matters. This is something that should be discussed carefully before the offer is written.

The answer depends on the loan structure, the down payment, the appraised value, and whether the buyer has any appraisal gap commitment in the contract.

A buyer may need additional cash if:

This is why I want my buyers to know their true cash comfort zone before writing an offer.

The question is not just, “Can you qualify for the loan?”

The better question is, “If the appraisal comes in low, how much additional cash can you comfortably bring in without putting yourself in a bad financial position?”

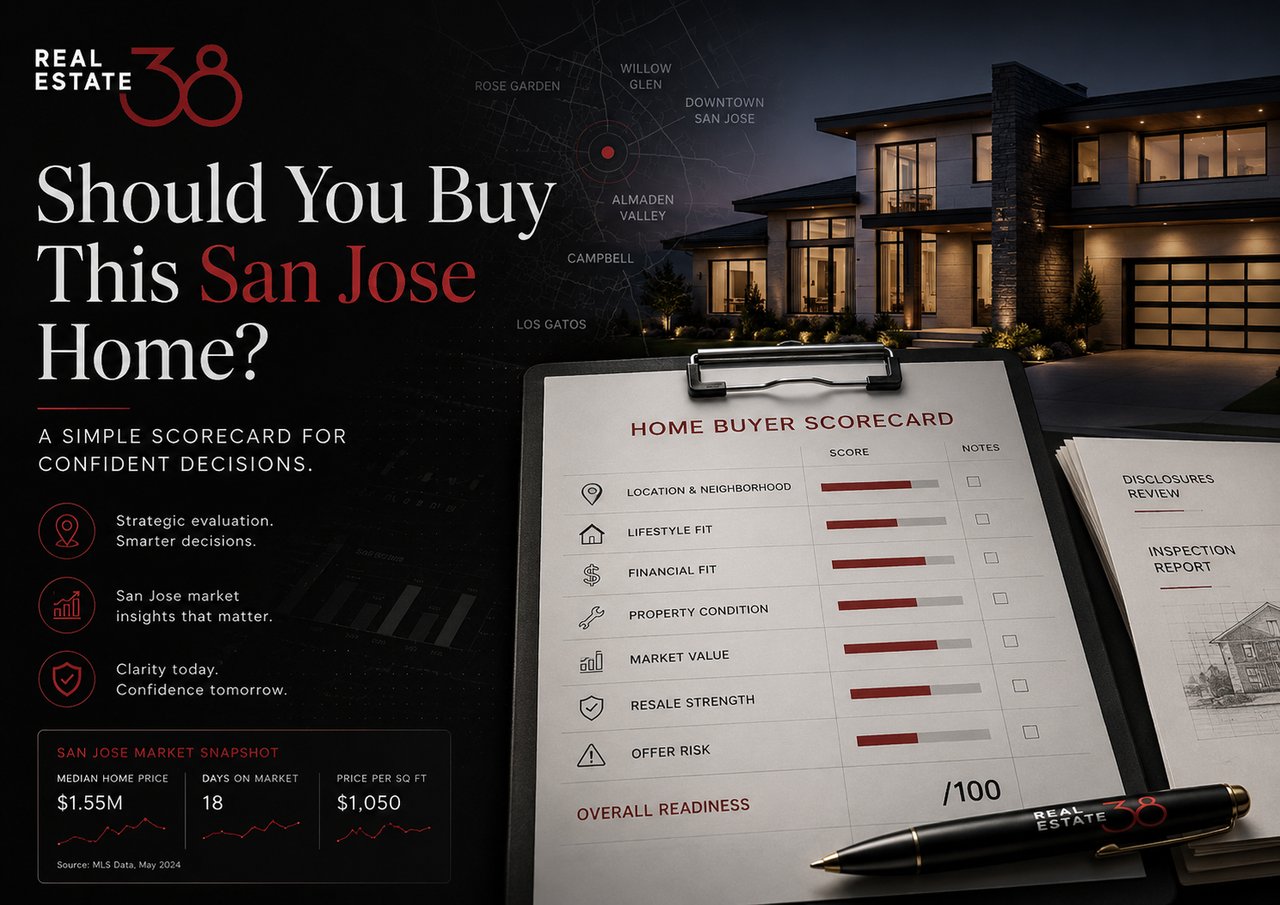

Before writing an offer, we need to study the comparable sales.

Comparable sales, often called comps, are recent sales that help support the value of the property. In San Jose, I look at factors such as:

This is where local knowledge matters.

A comp in Willow Glen may not tell the same story as a comp in Blossom Valley. A Berryessa single-family home may not appraise the same way as a Downtown San Jose condo. An Almaden Valley property with strong schools may behave differently than a townhome near a busy corridor.

The more precise the comp analysis, the better the offer strategy.

Not all San Jose properties carry the same appraisal risk.

Single-family homes can be easier to compare when there are enough recent neighborhood sales. But appraisal risk can increase when the home is heavily remodeled, expanded, located on a premium lot, or in an area with very limited recent sales.

Townhomes often depend on the floor plan, community, HOA, condition, and recent sales within the same or similar developments. A beautifully updated townhome may sell above older comps, but the appraisal still needs support.

Condos can be more sensitive to recent sales within the same complex. If one unit sold low due to condition, motivation, or timing, it may affect the appraisal conversation even if the subject unit is better.

This is why I evaluate appraisal risk differently depending on the property type.

A remodeled home may attract strong buyer demand, but the appraisal still needs data.

If the recent comps are older, outdated, or less desirable, the appraiser may not fully match what buyers are willing to pay for the upgraded home.

Unique homes can also be more complicated. This includes homes with:

These homes can still be great purchases, but the appraisal strategy needs to be thought through before the offer is submitted.

The best time to reduce appraisal risk is before writing the offer.

Here is what I help my buyers do:

A strong offer is not just aggressive. A strong offer is informed.

If the appraisal comes in low, buyers may have several options depending on the contract and financing.

The buyer can ask the seller to reduce the price to the appraised value or meet somewhere in the middle.

This is not guaranteed. If the seller has backup offers or the market is competitive, they may push back. But in some cases, renegotiation is possible.

The buyer may choose to cover the appraisal gap with additional cash.

This can work if the buyer has the reserves and feels comfortable with the value. But buyers should be careful not to drain all available cash just to force the deal through.

The lender may allow a reconsideration of value. This usually means submitting relevant comparable sales or pointing out possible errors in the report.

This does not always change the value, but it can help if the appraisal missed important data.

Sometimes the lender can adjust the loan structure, down payment, or program to help the buyer move forward.

This is why communication with the lender is critical. A strong lender should not disappear when the appraisal gets complicated.

If the buyer has the right appraisal protection in place and cannot reach a solution, canceling may be an option.

This is why the contract language matters. The earnest money outcome can depend on whether the buyer kept or removed the relevant protections.

Earnest money is one of the biggest reasons buyers need to understand appraisal protection.

If a buyer keeps an appraisal contingency and the home does not appraise, the buyer may have a path to cancel and protect the deposit, depending on the contract terms.

If a buyer removes or waives appraisal protection, then a low appraisal may not give them the same ability to cancel without risk.

This is not something to figure out after the appraisal comes in. It needs to be discussed before the offer is written.

At Real Estate 38, we help buyers evaluate appraisal risk before they commit.

That includes:

In a market like San Jose, you need more than enthusiasm. You need a strategy.

Do not wait until the appraisal comes in low to start thinking about appraisal risk.

If you are preparing to write an offer, ask these questions first:

The goal is not to scare buyers. The goal is to help buyers compete with their eyes open.

A low appraisal does not always kill a San Jose real estate deal, but it can create pressure if the buyer is not prepared.

The best protection is a smart strategy before the offer is written.

That means understanding the home, the comps, the lender’s requirements, your cash reserves, the level of competition, and the risk you are willing to take.

If you are buying in San Jose, especially in a competitive situation, I would rather help you analyze appraisal risk before you write the offer than try to fix a preventable problem later.

Before you make your next offer, contact me and my team at Real Estate 38. We will help you understand the appraisal risk, protect your cash, and compete with a smart strategy instead of guessing.

For more guidance, learn about buying a home in San Jose, explore current homes for sale, compare San Jose neighborhoods, or meet Zaid Hanna and the Real Estate 38 team.

Zaid Hanna

408-515-1613

www.re38.com

Stay up to date on the latest real estate trends.

June 10, 2026

June 8, 2026

June 5, 2026

May 29, 2026

May 28, 2026

May 18, 2026

You’ve got questions, and we can’t wait to answer them.