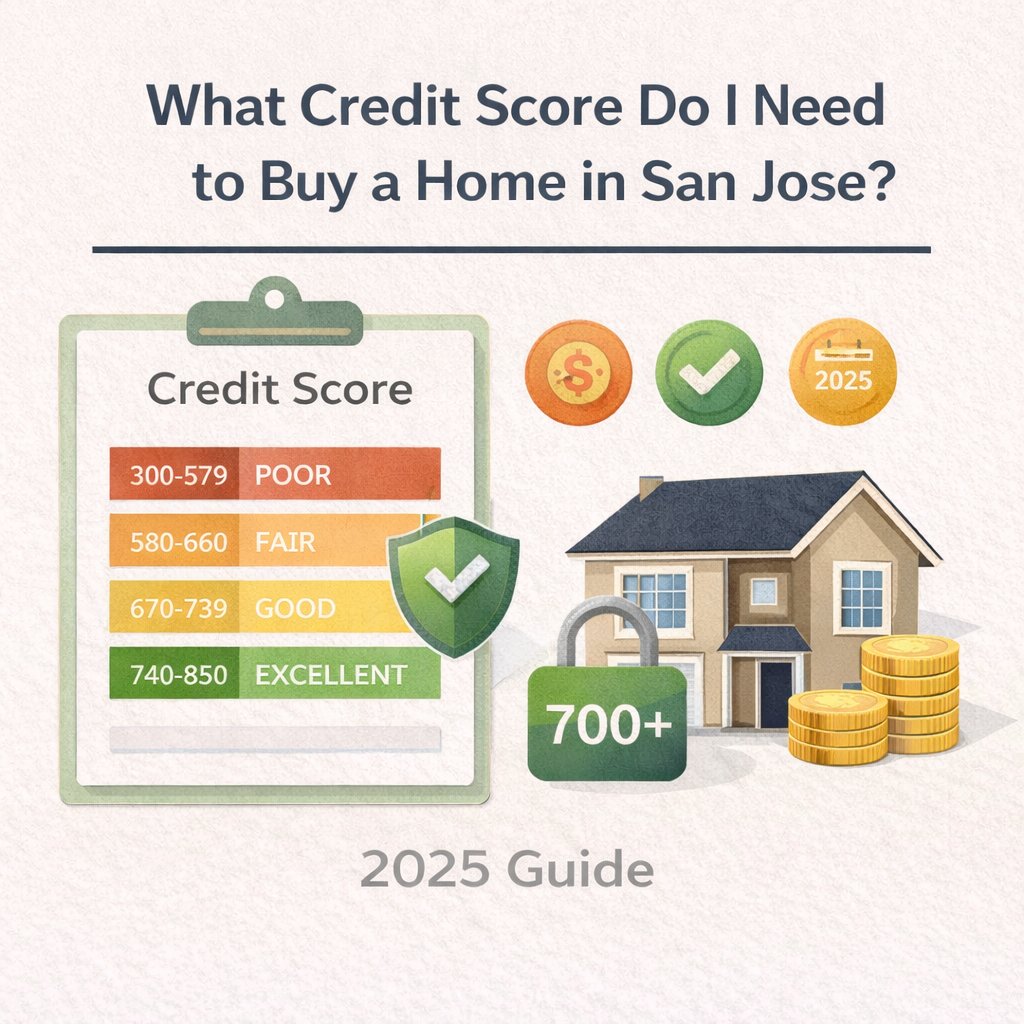

What Credit Score Do I Need to Buy a Home in San Jose?

Home Loans, Mortgage Rates & Affordability Guide

Home Loans, Mortgage Rates & Affordability Guide

One of the most common reasons buyers delay purchasing a home is uncertainty about their credit score.

I hear this all the time:

“I don’t think my credit is high enough.”

“I should probably wait another year.”

“I don’t want to talk to a lender yet.”

The reality is that many buyers qualify sooner than they think — especially when they understand how different loan programs work in a high-cost market like San Jose.

This guide explains what credit score you actually need, how credit impacts your loan options, and what to do if your score isn’t quite where you want it yet.

For a full overview of financing fundamentals, start here:

👉 https://re38.com/san-jose-home-loan-mortgage-guide

There is no universal minimum credit score to buy a home.

The score you need depends on:

loan type

down payment

income

debt-to-income ratio

reserves

overall credit profile

That said, there are general guidelines that help buyers understand where they stand.

Minimum: ~620

Better rates typically start around 680–700

Most common loan type in San Jose

Conventional loans offer flexibility and strong seller perception, especially in competitive markets.

Minimum: 580 (sometimes lower with larger down payment)

More forgiving of past credit issues

Mortgage insurance required

FHA loans can be helpful for first-time buyers, but may be less competitive in tight San Jose markets.

No official minimum set by VA

Most lenders prefer 620+

No PMI

Excellent rates

VA loans are a powerful option for eligible buyers and can be very competitive when structured properly.

Typically 680–720+

Strong income and reserves required

Common in San Jose due to higher home prices

For jumbo buyers, credit score impacts not just approval — but pricing and terms.

In San Jose, many buyers aim for:

680+ for solid approval options

700+ for better rates and flexibility

740+ for top-tier pricing

However, buyers with lower scores can still qualify depending on income, down payment, and overall strength.

Your credit score directly impacts:

interest rate

monthly payment

long-term cost of borrowing

Even a small difference matters.

For example:

A 20–40 point improvement can save hundreds per month

Over time, that can mean tens of thousands in interest savings

That’s why timing and preparation matter.

High income can sometimes offset a lower credit score.

In San Jose:

strong W-2 income

RSUs or bonuses

stable employment

can help buyers qualify even if their credit isn’t perfect.

This is especially common among tech professionals.

False. Many buyers purchase with scores in the mid-to-high 600s.

Closing accounts can actually hurt your score.

Checking your own credit does not hurt your score.

Time and consistent behavior matter more than one mistake.

If your credit score is slightly below where you want it to be, simple steps can help:

pay down balances (not close accounts)

avoid new credit inquiries

keep utilization below 30%

make all payments on time

work with a lender on a credit improvement plan

Even 30–60 days can make a meaningful difference.

Remember, approval depends on:

income

debt-to-income ratio

down payment

reserves

loan type

Credit score matters — but it’s not the whole story.

For the full buying roadmap, review:

👉 https://re38.com/san-jose-home-buying-process-guide

Instead of guessing where you stand, let’s look at your full picture.

I help buyers:

understand real qualification thresholds

connect with trusted local lenders

create a realistic buying timeline

avoid unnecessary delays

👉 Reach out here:

https://re38.com/contact

A short conversation can give you clarity and a plan — even if you’re not ready to buy yet.

Zaid Hanna

408-515-1613

www.re38.com

Stay up to date on the latest real estate trends.

August 6, 2026

July 31, 2026

July 27, 2026

July 24, 2026

July 24, 2026

July 22, 2026

You’ve got questions, and we can’t wait to answer them.